By MOTIFE Insights, 24 September 2025

The rules of personal income taxation can differ from one country to another, so let’s start by defining what they are in Poland. Net income of employees in Poland, also called “take-home earnings” (in Polish na rękę), is calculated from gross income by taking into account personal income tax rates, social security contributions as well as tax-deductible costs. Tax-deductible costs reduce the amount of personal income tax.

The standard amount of tax-deductible cost is low and is a lump sum of approx. 250 PLN / 56 EUR per month (or 300 PLN / 67 EUR per month if employees work in a different town than where they live). It covers the assumed standard monthly costs related to the employment (for instance, the employee’s expenses for their commute to work).

Check out also: 2026 Krakow IT Market Report

Not all creators may enjoy this benefit – there is a list of types of creative works that are eligible. The list includes, among others, computer programs, music, or scientific literature.

This regulation applies to freelance workers who work according to a “specific work agreement” (umowa o dzieło) or “services agreement’’ (umowa o świadczenie usług / umowa zlecenie).

However, it can also apply to the salaried employees that created copyrighted work, such as university workers, graphic designers, and software developers that are employed, for work requiring thorough analysis and reporting procedures.

When applied, the tax-deductible costs scheme for creative work allows employees to reduce their personal income tax and therefore increase their net income (“take-home earnings”). Without increasing employer costs, the employee’s net income can increase by as much as 13% per year.

With that, employers can benefit in the following ways:

This scheme has gained popularity throughout the IT industry in Krakow with large international software companies, having engineering teams of 1000+ people, utilizing its benefits. The scheme is also being applied in smaller IT firms.

We have prepared a scheme simulator (Google Sheet). Feel free to save your own copy of the scheme simulator and adapt the fields to reflect your organization’s scope.

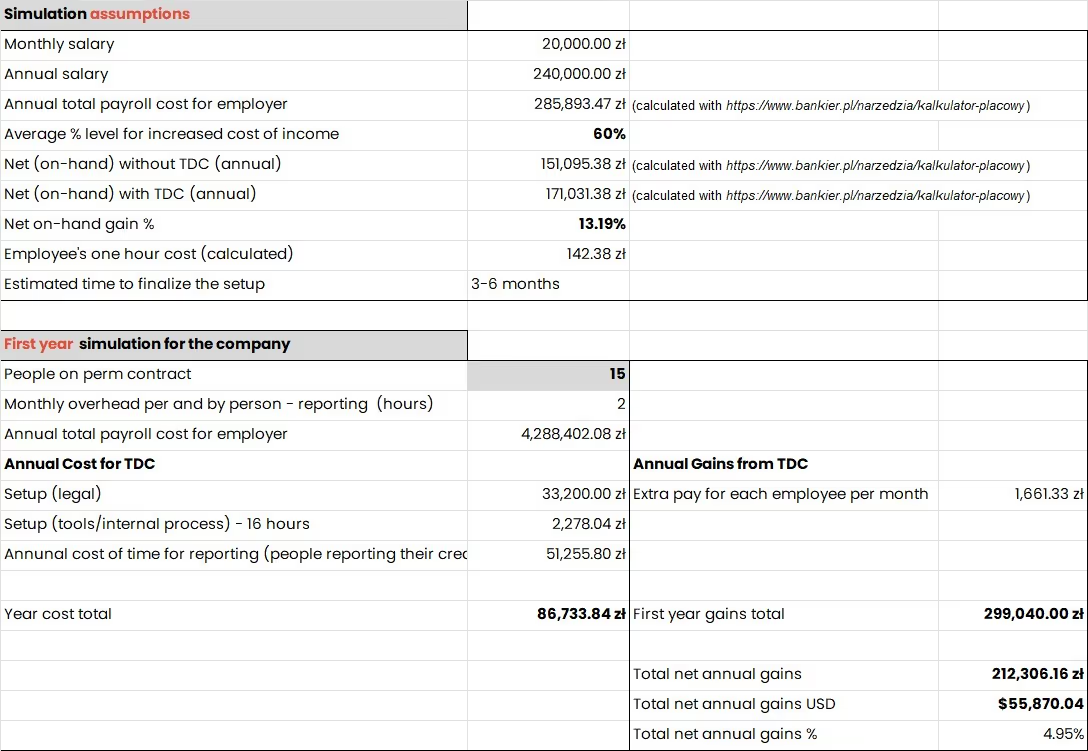

In this particular example, we simulated the attractivity of the scheme for a Polish subsidiary that employs 15-20 software engineers on full-time employment contracts, where the average gross remuneration is 20 000 PLN per month.

Figure 1: Tax-Deductible Costs (TDC) in Poland – scheme simulator for IT companies

To utilize Tax-deductible costs in your organization, the following points will need to be addressed:

How to proceed?

Who? Most companies use law firms or local operational partners who have experience in the subject to help them go through this process to make sure it is executed smoothly and to assure compliance with legal regulations. In addition to this, the process requires cooperation between several parties, including engineering and HR in the organization as well as with the payroll company.

How long? The entire process can take up to 6 months (though it could be in theory faster since the Ministry of Finance has issued on 15 September 2020 a general interpretation on TDC rules, replacing the application to tax authorities for an individual interpretation in place previously).

How much does it cost? The estimated legal fees are approximately 10 000 EUR and can be broken down and viewed under 5 categories:

You should also have to plan for some hours spent within your organization (we estimate setup time on 1st year to ca. 16 hours, and 2 hours/employee/month for the reporting on their own creative tasks).

1. Only work categorized as “creative works” qualifies. Work records have to be detailed and document the creative tasks. Employees need to create a copyrighted work.

2. Payroll for an employee may change month to month. Detailed work records need to be created each month. This means that an employee may have a varying amount of work that qualifies so their payroll will change month to month.

3. Not all employees will be able to benefit. There will be discrepancies and it is crucial to plan ahead an approach towards the departments that are not eligible (I.e. Sales, Finance, Customer Service).

4. Additional workload for HR and Payroll. Administration of the scheme is an overhead – detailed tracking of work is required. This information has to be consolidated by HR and Payroll; employees pay will vary depending on the work they are doing each month.

1. Why might the lack of an implemented creative tax scheme be considered as a missed opportunity for attracting talents?

When a new IT company opens its office in Poland, it gets a bonus for being a new player in the market. After a year or two, it has to compete with other employers on the market. If a candidate has two similar job offers in hand, he will likely choose the one that offers him a higher net income. Moreover, not having a creative tax scheme in place may raise questions such as ‘’Why don’t they have it?’’. To a certain extent, it impacts the employer branding of a company.

2. Could employees refuse offers or leave a company as a result of not having this scheme in place?

For employees and candidates, having a wide range of choice between the IT companies who have the scheme implemented opens up the possibility of movement within the industry and search for higher income.

3. What is implementation costs of TDC for an employer?

Legal advisory services, cost of HR engagement in the implementation process (e.g. answering employees’ questions regarding 50% costs, assisting in introducing amendments to employment contracts, ensuring the smooth running of the process), cost of payroll process adjustments, possible increased month-to-month payroll costs, cost of verification of new job positions in terms of possibility of 50% costs application, cost per hour rate of legal counsel.

4. What are the HR issues if some employees are not working on TDC qualifying projects and the person next to them is and receives a tax benefit? How can this be resolved – assuming as with all organizations that employees are likely to discuss pay arrangements with each other?

There is no issue from an HR perspective, the process implications and job position audit clearly indicate what kind of creative work needs to be performed, it is therefore governed by tax regulations and doesn’t apply to unequal treatment.

5. Could the Tax-Deductible Costs scheme be an efficient tool to encourage contractors to move from B2B contracts to employment contracts?

The Polish government’s position is that B2B contracts are accepted as a form of engagement. However, similarly to the UK, the government is from time to time talking about changing this situation, so that contractors who are only delivering services to one company are considered to be in fact employees. The following B2B contractors might be targeted by the government:

Moving from B2B contracts to employment contracts may address the risk to be targeted, and creative tax might help the company to optimize costs related to transition.

6. What does the copyrighted works tracking process look like?

Procedures for verification if an employee created any copyrighted works include reports confirming the creation of copyrighted works and an indication of the place where these are stored. In addition, in order to avoid any doubts and to determine precisely the duties of employees, an unambiguous provision imposing a duty on employees to create specific copyrighted works under their employment relationships should be introduced to the employment contract.

7. Who determines whether work qualifies each month for the benefit? Who is responsible for that determination when proven to be incorrect? Do we recover errors from the employee?

At least one work item must be created so that the employee is eligible for 50% deductible costs. Each role has a list of works associated that qualify. For developers it is automatic – any code that they create qualifies as each line of code can be a copyrighted work.

The direct supervisor/manager would be responsible for the verification of the work performed and must approve a report with the summary of work created (on a monthly basis). Exceptions when no copyrighted work was produced in a specific month would be reported to the payroll company. Should a tax audit be performed, only the existence of the work exists (and not the content of the works itself).

8. What happens if someone is sick or on holiday – Are their take-home earnings reduced as they won’t have been working on eligible projects?

Sick leave or holiday will impact copyright cost, tax, and salary. Tax-deductible costs will be applied when the employee works at least 1 day during the month and creates at least one copyrighted work, but they will be applied to the pay for work only, not to the leave/sick leave part of the salary. On the other hand, in the worst-case scenario, when an employee is absent for a whole month, take-home earnings decrease to the level of the situation when copyright costs are not applied.

.png)

If you are looking for information about setting up your presence in Poland, download our 2026 Krakow IT Market Report.

If you are interested in alternatives to outsourcing, contact us at MOTIFE to learn more.

If you are looking for interesting job opportunities in tech companies in Krakow and remote, check out open roles at motife.com/jobs.

Explore essential data on Poland's tech landscape.

View all job offers

Download the report

Read the full client story